Bonuses: Short-Term Incentives

A short-term incentive or “bonus” may be used in several ways, but each of these ways requires something to have been achieved. That something may centre on an individual, a team, a task or project, or the company as a whole. The nature of the event for which a reward is provisioned may range from the nebulous to the precise. Bonuses cost money – usually a lot of money if they are to be significant to the recipient. Despite this high cost, senior management often spends far less time taking decisions over bonus planning than they would over an investment of a fraction of the cost.

Bonuses: Short-Term Incentives

A short-term incentive or ‘bonus’ may be used in several ways, but each of these ways requires something to have been achieved. This may centre on an individual, a team, a task or project, or the company as a whole.

The nature of the event for which a reward is provisioned may range from the nebulous to the precise.

Bonuses cost money – usually a lot of money if they are to be significant to the recipient. Despite this high cost, senior management often spends far less time taking decisions over bonus planning than they would over an investment of a fraction of the cost.

When Should You Pay a Bonus?

A bonus should be paid only when its payment meets some need within the company; where its payment will enhance value or prevent the destruction of value in the company. The stronger the link with demonstrable achievement, the greater the impact and the value obtained will be.

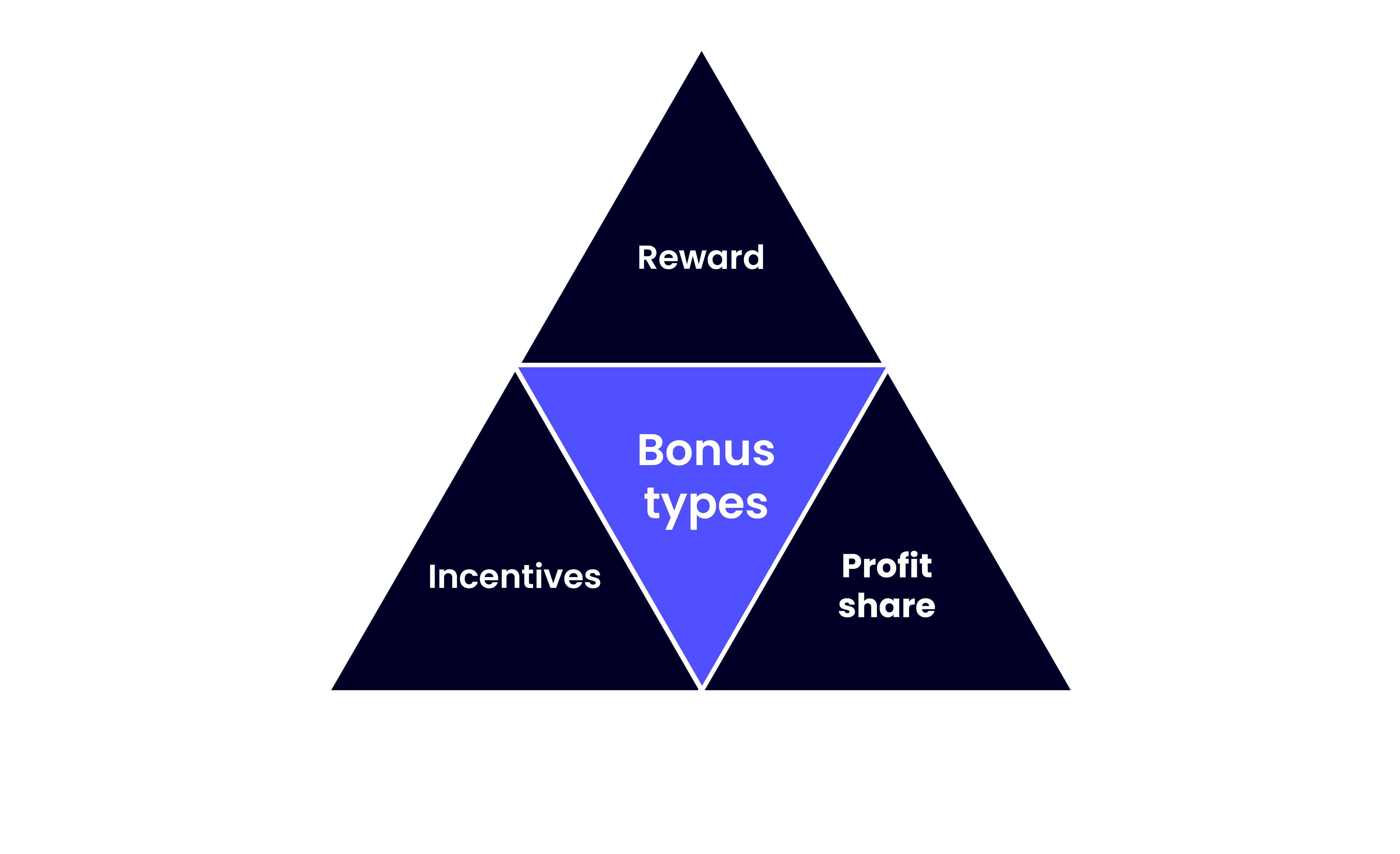

There are three possible uses of bonus: to reward employees, to incentivise them, or to enable them to share in the profits of the company. Each bonus use has different characteristics and, ideally, should be used in different situations.

To be effective, bonus plans should be clearly communicated, with clearly defined aims. Bonus schemes with confused objectives or those that try to meet all possible uses will most likely achieve none of their objectives and can be damaging to the organisation.

It should also be realised that a “one-size-fits-all” bonus is unlikely to be competitive and will only be effective in organisations that have a democratic philosophy such as the John Lewis Partnership, and even here such a bonus is percentage-based, not a flat cash value. Bonuses at different levels in an organisation often perform different functions. The time horizon of the employee group is one factor here and this in turn is often related to seniority.

Bonus Types

Profit Share

- Warm feeling generated when paid out, but employees are not directed at specific actions, so linkage is small

- Only normally awarded annually, and often long after the event as profits have to be audited

- Low-to-moderate pay-out, since these schemes tend to be all-employee based and direct contribution from any one employee is difficult to determine

Reward

- Payment is made after the event, in recognition of one, or multiple achievements. Since the size of the payment and the actions are not clear at the outset, there is some linkage, but this is moderate at best.

- Paid after the event, although this depends on its nature.

- Moderate-to-low pay-out – although demonstrable achievement has been displayed, corporate philosophy is likely to kick in and limit the size of the payment

Incentive

- Actions for which payment will be made are clearly set out, as is the expected payment. The connection with set goals can be very strong.

- Payment can be annual, or another regular period, to keep the incentive alive.

- Significant enough value to the individual in order to act as an incentive.

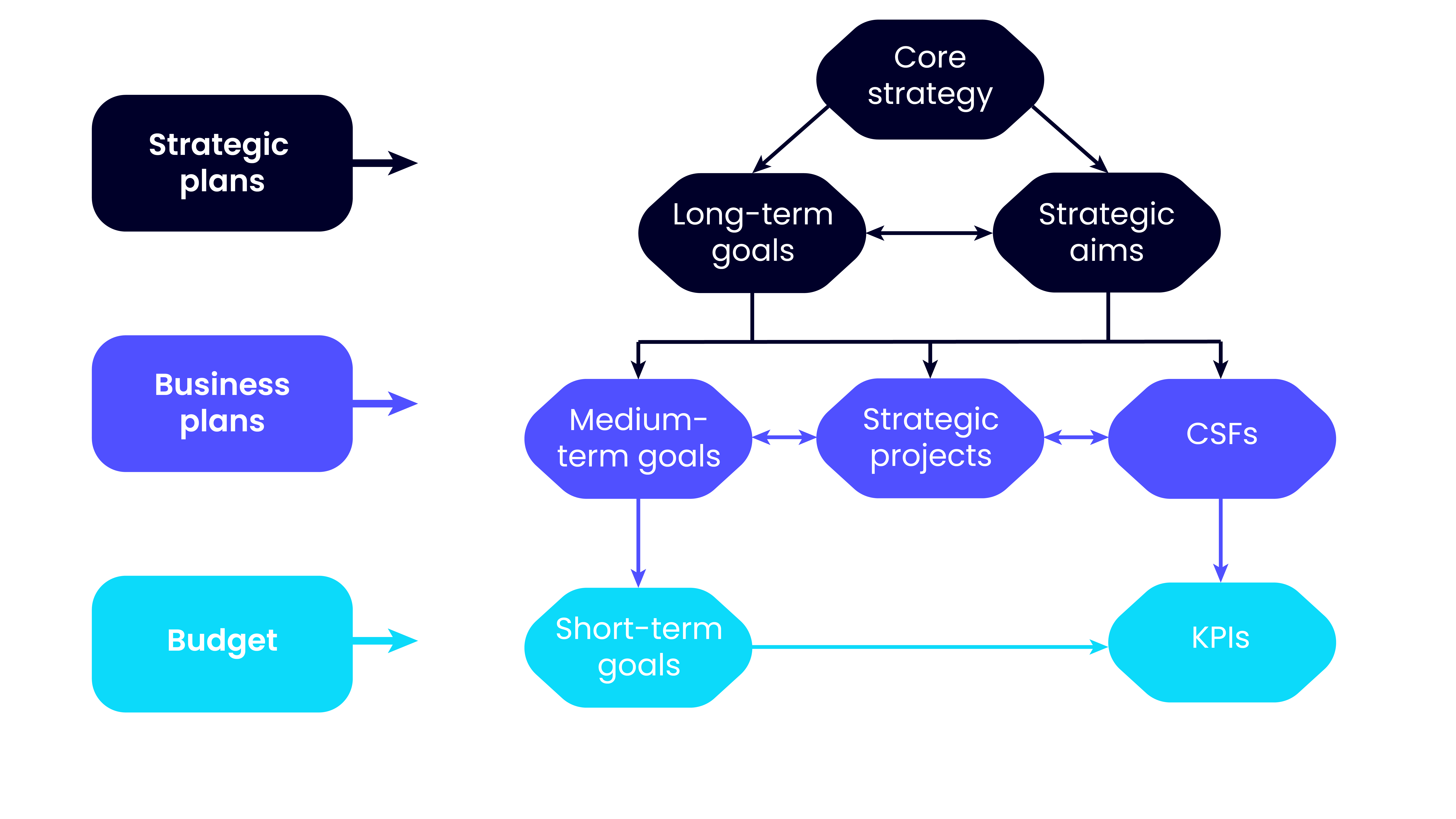

Linkages for a Strategic Planning Process

The point that must be considered is what you are trying to achieve through bonuses.

You can target actions, but beware that some of these might be targeted to the exclusion of others.

If you target someone on quality, quality is what you will get – but probably at the cost of something else.

Sales are relatively easy, provided you relate the amount of bonus or commission to some other desired goal such as profitability or capacity.

Starting with Strategy

A company that has a clear direction and a well thought out means of achieving that direction can target bonus payments to bring about the achievement of its strategic aims.

The diagram above looks at the linkages for a strategic planning process. Without a clear view on long-term goals, incentives can be unfocused, and actions may be rewarded that may or may not be in line with the company’s aims. Strategic aims of the company translate into measurable long-term goals.

In order to achieve the strategic aims, there are a number of factors that are critical. These are known as Critical Success Factors (CSF s), and they:

- Need to be focused on projects they can develop from and support

- Need medium-term goals against which to measure progress, which in turn form staging posts to ensure that quantifiable progress is being made to meet long-term strategy.

Short-term incentives should be directed at short-term actions and short-term goals should be established.

This is often what we do with the organisation’s budget. The measurement of achievement of those short-term goals is through a series of key performance indicators (KPI s) that in turn are derived directly from CSF s. This structure ensures that an incentive achieves something of value to the organisation. It either reaches a financial milestone or improves the ability of the organisation in some way.

Short-term incentives are often regarded as dangerous because they encourage actions for this quarter or this year that could damage the future of the company. An example would be a house-building company where a piece of land is sold to make a profit to flatter this year’s figures. The company makes a profit this year, but its land bank is important in that it is able to make more money from developing the land itself. The short-term action has reduced the ability of the company to make future profits, and since it is almost certain that the buyer is a competitor, it has weakened the competitive stance of the seller.

The lesson here is that an incentive for this company based on a single measure such as overall profit or return on capital could damage the long-term prospects of the company. The incentive needs to be aligned with the needs of the organisation. So, the message is simple:

- Know what your short, medium and long-term goals are.

- Design your bonus to target the achievement of those goals.