Creating a Corporate Budget

The purpose of a corporate budget is primarily to enable a company to track its financial progress over a specified period. A budget will normally be set for a year and reviewed at periods of a week, a month, or a quarter to ensure that the company’s progress is on its expected track. Getting this process right can play a crucial role in the financial success of your organisation.

Creating a Corporate Budget

There are essentially two types of approach to setting a budget:

-

A historically-based approach

-

A zero-based approach

In truth, most well-constructed budgets will contain elements of each approach, with the historical basis being the most common and useful for an existing enterprise.

The Historically Based Approach In this method, we project future revenues and costs on the pattern of recent years’ trading. Thus, we will look back and see the pattern of the revenues and costs by week or month and determine, with appropriate inputs from business leaders, the expected outrun for the equivalent future period.

The Zero-Based Approach (ZBB)

As its name suggests, this approach starts from a position of no costs and no revenues and each element of the budget is justified and challenged.

Each approach has its virtues, but ZBB can be more resource intensive and time consuming although it can create the most well-founded financial budgets as everything is considered and challenged.

Business Plans

A well-run business will normally consider what it wants and needs to achieve over the next several years and create plans and projects with associated forecast costs needed in order to fulfil those aims. These decisions will be articulated in a Business Plan and this should inform the annual budget and provide it with a structure from which to build.

Key Budget Elements

The key elements of a financial budget are:

-

Revenues

-

Costs

-

Investments

-

Financing

-

Credit Management and Cash Flow

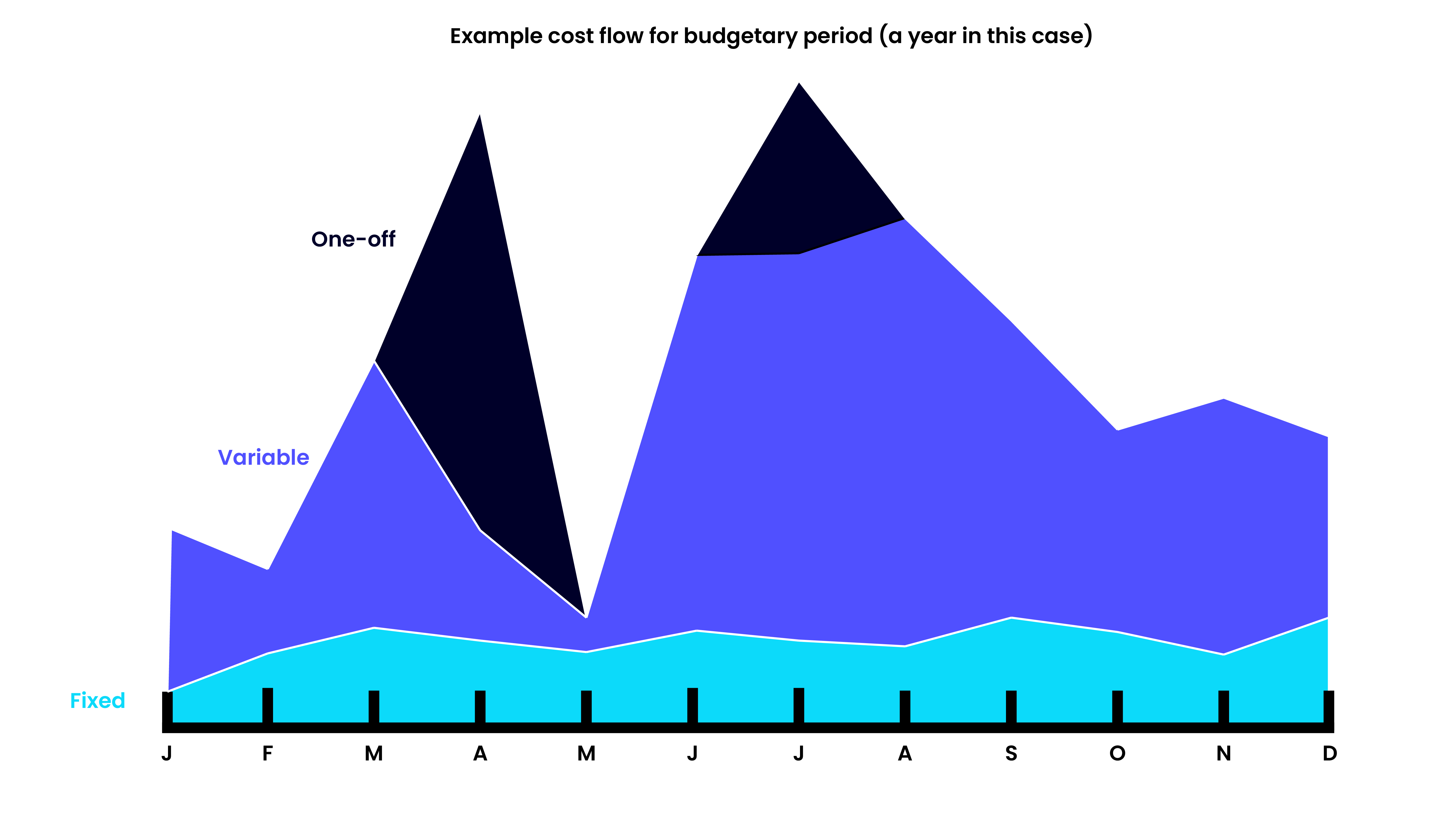

Types of Monetary Flows There are three principal types of monetary flow, which apply to both revenues and costs:

Fixed Flows

These are flows that are known with reasonable certainty for the budget period and are usually related to a fixed, contractual arrangement.

Examples would include revenue from maintenance contracts and costs of rent of premises. As these are relatively well-known it is generally wise to use these as the first entries into your budget.

Variable Flows

These are flows that come generally as the result of business activity. Most sales, not included in fixed flows, would fall under this category. Costs of raw materials, related to the budget period, which generally scale with the volume of production, also fall under this category. Projection of these flows will normally be based on their equivalents from the previous financial period where products or services exist in both periods.

Variable flows will be based on expected activity that has been planned by the business for the budget period. While a Finance function may be able to do reasonable projection of these flows based on previous activity, the various business functions will have to confirm and amend the raw projections based on their current knowledge of the market and the assumptions that have gone into their business planning.

One-off flows

As their name suggests, these monetary flows are neither fixed nor variable, but come from expected transactions that, while they may be known in quantum and time are significant in scale and not likely to be repeated.

Examples would include the sale of capital plant and machinery or the freehold or lease on a business premises. Equally, a diminution in value of stock of goods held or an expenditure for new plant and machinery would qualify under this label.

Creating the Budget

In order to create our financial budget, we need to consider all costs and revenues that have occurred in recent years of trading.

It will be necessary to list all sources of cost and revenue from prior trading and determine for each for its flow-type, its likely quantum and its likely timing during our budget period.

Beware when considering the timing of flows that costs might be brought forward, or revenues delayed due to changes in the external environment or due to changes in the internal policies of the organisation. To do a budget that reflects the financial cycles of the business, one must be have intimate knowledge of the business and its component parts.

Budgets need not be complex but the greater the detail in a budget the more likely it will be that one can identify which specific elements are drifting from the budgeted line. This will enable the company to take action to correct the negative occurrences or exploit the positive.

As the compiler of a budget, it is best if one requests information in similar format and detail (a template) from all business functions that are to submit budgets. This ensures that you have the right level of information to bring together and a consistent basis to track the progress of the organisation through the budget period.

All flows should be accounted for in the template that you provide to each contributor, as this will ensure that all items are captured, including those unexpected items in functional budgets that assumptions of content might miss – for example, revenue in a function expected to be cost only or financing costs in a function that would not normally have them.

Making the Budget a Business Tool

A budget can be seen as primarily useful for tracking financial flows so that the company can see where its costs and revenues arise from and how they compare with expectations.

In order to make the budgeting process useful to the company, those flows need to be turned from data to information. In order to achieve this, the principal tasks that need to be done are:

1. Apply the accounting policies of the organisation

Applying accounting policies and practices to the flows creates a set of information that represents a measure of the position the company represents to the outside world – its published financial records. With this viewpoint on the budget, the company can see where it is compared to what it may have told its shareholders and be prepared with suitable information when external reporting time occurs.

2. Consider the flows that affect cash and those that do not

Cashflow is extremely important to all businesses. If there is insufficient positive cash generation from the company’s operations in any period of the budget, then short-term financing may be needed to ensure that it can continue to operate. In order to project cash flow, the size and timing of financial flows need to be considered.

Revenues may be booked but most often these will not turn into cash immediately.

In most normal operations both costs and revenues will likely be filtered through a set of terms for payment and this may delay the cost by months after it has been booked or incurred.

Therefore, credit terms with suppliers and customers should be examined to get as accurate as possible a handle on when cash will likely enter and leave the business.

Where the budget projections show short falls in cash that exceed the on-hand resources, the company will be able to plan to negotiate a credit facility with its bankers.

Conversely, where there is significant positive cash flow, the company can plan for the its use – perhaps by further investment in short term marketing to further boost revenues or by using it to make financial investments that will provide a boost to profitability.

3. Set triggers for the budget flows

Some variation in actual monthly flows versus projected flows is inevitable.

What often helps in an organisation is some mechanism to determine which pieces of information to apply focus onto and which not.

This is best done by setting some variation parameters to the individual flows.

These parameters will normally be the percentage of the budgeted flow by which the actual out-turn varies by the month and cumulatively for the number of months of the budget period under review.

The percentages applied to force triggers will not be uniform across the flows. In order to consider the size of variation that should force a trigger, it is normal to consider the certainty of the flow and the type of flow.

For example, an expected fixed cost might have a low variation percentage because it should be well known both in quantum and timing. This flow would be brought to the company’s attention only if it did not behave within a few percentage points of its projection.

A variable flow on the on the hand might only trigger at a higher percentage variation as its timing and quantum are less certain. Triggers are normally best displayed visually in a budget – either by exception reporting (showing only those floes that are under or over projection in excess of the variation percentage) or by using a visual flagging system for exceptions with all flows shown.

Conclusion

Budgets are useful tools to enable a company to achieve its short-term goals.

Properly constructed, a budget is a valuable business toll and not merely a financial exercise.

A swath of management information can be gleaned from a properly analysed budget by looking at expectations and trends enabling the business to take actions to exploit opportunities and mitigate negative occurrences.