Balanced Scorecard

A Balanced Scorecard approach is to take a holistic view of an organization and co-ordinate MDI s so that efficiencies are experienced by all departments and in a joined-up fashion.

Kaplan and Norton:

Organisational Performance Management Tool

In the beginning, was darkness. We went to work, did our job (well or otherwise) and went home - day in and day out. We did not have to worry about targets, annual assessments, metric-driven incentives, etc. Aahh… life was simple back then.

Then there came light. Bosses everywhere cast envious eyes towards our transatlantic cousins whose ambition was to increase production and efficiency year-by-year. Like eager younger siblings we trailed behind them on the (sometimes) thorny path to enlightenment.

Early Metric-Driven Incentives - MDI s - were (generally) focused on the financial aspects of an organisation by either claiming to increase profit margins or reduce costs. They were not always successful, for instance,å driving down costs could sometimes be at the expense of quality, staff (lost expertise) or even losing some of your customer base.

Two eminent doctors, Robert S Kaplan and David P Norton, evolved their Balanced Scorecard system from early MDI s and jointly produced their (apparently) ground-breaking book in 1996.

Many other ‘gurus’ have jumped on the Balanced Scorecard wagon and produced a plethora of books all purporting to be the ‘Definitive’ book on Balanced Scorecards. Amazon.com shows over 4,000 books listed under Balanced Scorecards, so take your pick - and your chances!

Definition

What exactly is a Balanced Scorecard? A definition often quoted is: ‘A strategic planning and management system used to align business activities to the vision statement of an organisation’. More cynically, and in some cases realistically, a Balanced Scorecard attempts to translate the sometimes vague, pious hopes of a company’s vision/mission statement into the practicalities of managing the business better at every level.

A Balanced Scorecard approach is to take a holistic view of an organisation and co-ordinate MDI s so that efficiencies are experienced by all departments and in a joined-up fashion.

To embark on the Balanced Scorecard path an organisation first must know (and understand) the following:

- The company’s mission statement

- The company’s strategic plan/vision

Then

- The financial status of the organisation

- How the organisation is currently structured and operating

- The level of expertise of their employees

- Customer satisfaction level

The following table indicates what areas may be looked at for improvement (the areas are not exhaustive and are often company-specific):

Example Factors

| Department | Areas |

| Finance | Return On Investment

Cash Flow

Return on Capital Employed

Financial Results (Quarterly/Yearly) |

| Internal Business Processes | Number of activities per function

Duplicate activities across functions

Process alignment (is the right process in the right department?)

Process bottlenecks

Process automation |

| Learning & Growth | Is there the correct level of expertise for the job?

Employee turnover

Job satisfaction

Training/Learning opportunities |

| Customer | Delivery performance to customer

Quality performance for customer

Customer satisfaction rate

Customer percentage of market

Customer retention rate |

Once an organisation has analysed the specific and quantifiable results of the above, they should be ready to utilise the Balanced Scorecard approach to improve the areas where they are deficient.

The metrics set up also must be SMART (commonly, Specific, Measurable, Achievable, Realistic and Timely) - you cannot improve on what you can’t measure! Metrics must also be aligned with the company’s strategic plan.

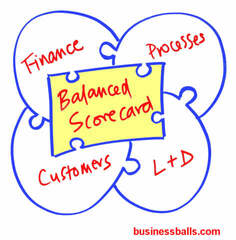

A Balanced Scorecard approach generally has four perspectives:

- Financial

- Internal business processes

- Learning & Growth (human focus, or learning and development)

- Customer

Each of the four perspectives is inter-dependent - improvement in just one area is not necessarily a recipe for success in the other areas.

Implementation

Implementing the Balanced Scorecard system company-wide should be the key to the successful realisation of the strategic plan/vision.

A Balanced Scorecard should result in:

- Improved processes

- Motivated/educated employees

- Enhanced information systems

- Monitored progress

- Greater customer satisfaction

- Increased financial usage

There are many software packages on the market that claim to support the usage of Balanced Scorecard system.

For any software to work effectively it should be:

- Compliant with your current technology platform

- Always accessible to everyone - everywhere

- Easy to understand/update/communicate

It is of no use to anyone if only the top management keep the objectives in their drawers/cupboards and guard them like the Holy Grail.

Feedback is essential and should be ongoing and contributed to by everyone within the organisation.

And it should be borne in mind that Balanced Scorecards do not necessarily enable better decision-making!

See also

-

Bloom’s Taxonomy of Learning Domains (Educational Objectives)

-

Employment termination, dismissal, redundancy, letters templates and style

-

Performance appraisals - process and appraisals form template

Authorship/Referencing

© Sandra McCarthy and Alan Chapman 2008-2013.